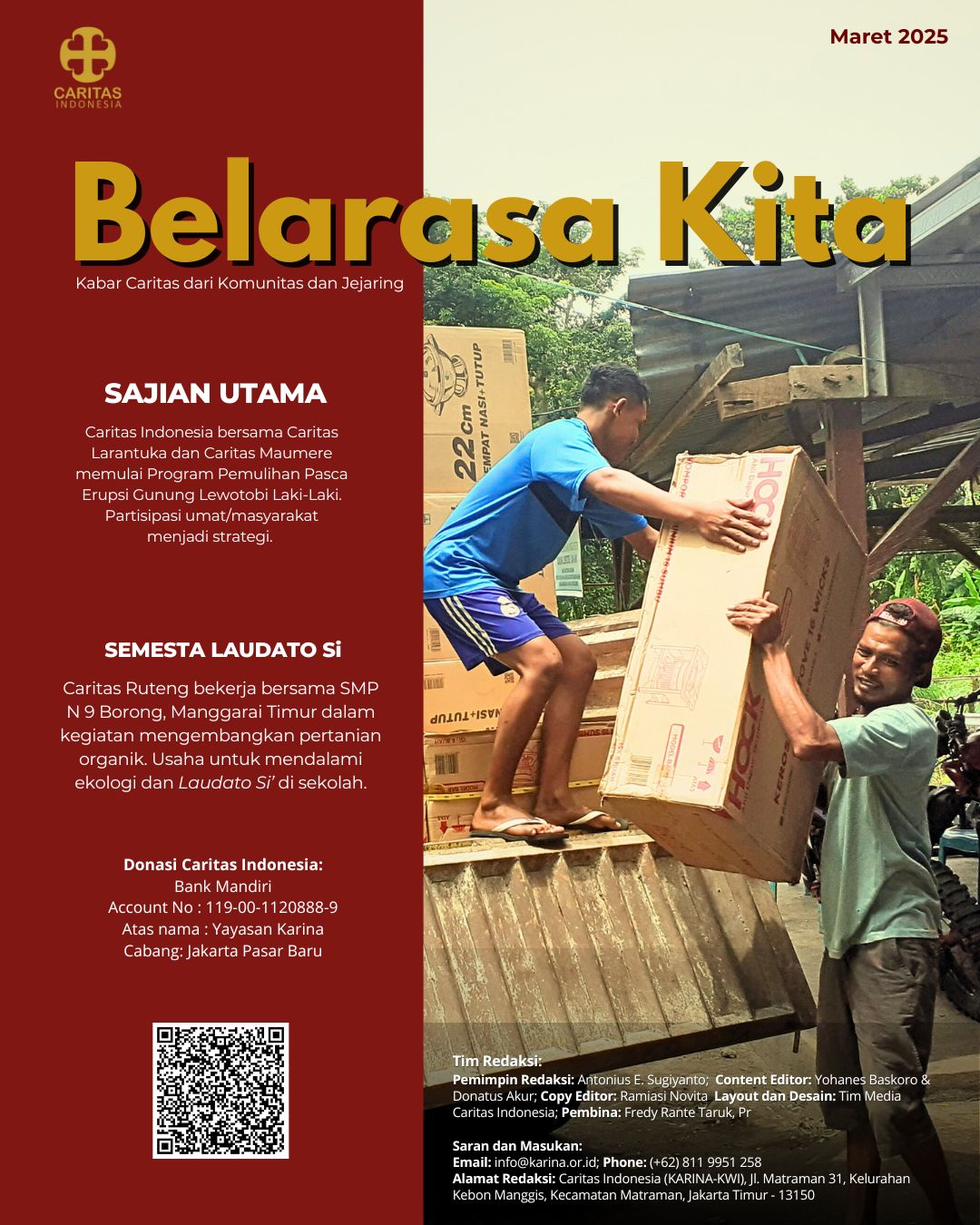

CARITAS INDONESIA

Caritas Indonesia (Yayasan KARINA) secara hukum didirikan pada tanggal 17 Mei 2006 dan merupakan lembaga kemanusiaan resmi milik KWI (Konferensi Waligereja Indonesia) dengan mandat sebagai pusat koordinasi, fasilitasi dan animasi Lembaga Sosial-Pastoral Gereja Katolik di Indonesia dalam menjalankan misi kemanusiaan, terlebih untuk membantu para korban bencana alammaupun bencana